Very high individual costs of participating in ObamaCare make most government subsidized plans useless. Politicians promoting the program want to include you in their numbers of covered individuals and hope you just don’t recognize the situation until it’s too late.

An article in USNews & World Report 5 Dec 2016 documents what ObamaCare costs are to individuals. In Fort Lauderdale, Florida, for example, the cheapest Bronze plan available for a 60-year-old woman who doesn’t smoke is an HMO for $582 a month, with a $7,150 deductible, which comes out to $14,134 in medical costs before any services are covered. That’s nearly 30 percent of before-tax income for someone who makes $48,000 a year. The premiums alone are 15 percent of income.

For a couple, both 60, making $65,000 a year, premiums would be $1,164 for that plan, with a $14,300 family deductible. The $13,968 premiums would eat up more than 20 percent of their income, and out of pocket costs are $28,268 (43 % of their income) before insurance kicked in. This is insane for anybody to consider budgeting for this!

A 25-year-old would pay $215 a month for the same plan, and would be $16,880 out of pocket before insurance pays a dime.

A family of four, comprised of two 40-year-old adults and two children, would pay $820 a month with a $14,300 family deductible. $24,140 out of pocket.

People who like the Obama-care program claim this is “insurance coverage” and quote how many more people are now “covered”. That’s a joke – covered as in their name is on a piece of paper or in a data base, but not covered if you think that means saving money on health care. For politicians, it allows them to claim success while really providing almost nothing.

In fact, there are only 3 parameters to adjust in the health care equations: the quality of care, the accessibility & speed of care, and the cost of care. There is no way to add millions more people into the health care system who are net consumers and say the quality and accessibility remain the same.

The high premium and deductible costs destroy accessibility for the very people the law says it helps. And, of course, the architects of the program knew that high out of pocket expenses would make people not sign up, which is why they had to penalize people with an IRS fee or tax to make them obey and become part of the system. If many new “covered” people are charged a lot of money and given very little in return – viola! – the program might be able to financially survive, while at the same time politicians can claim you’re now better off because you’re “covered”.

With mostly useless “coverage” like that documented above, no wonder many are just paying the penalty!

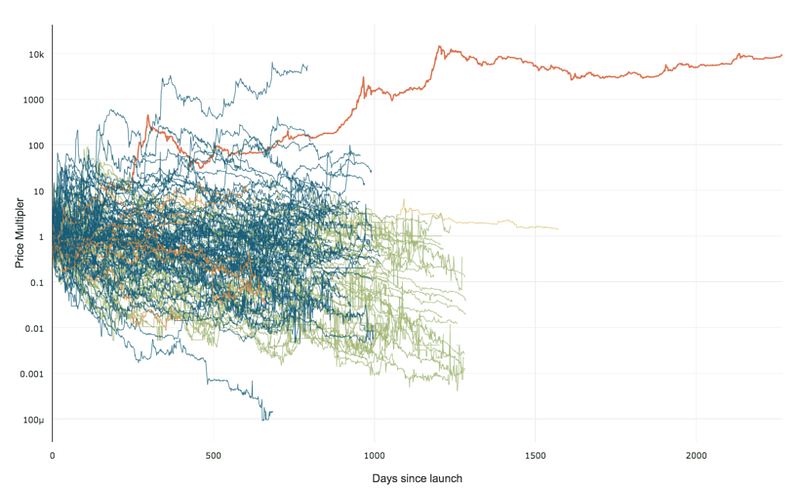

99% of ICOs Will Fail

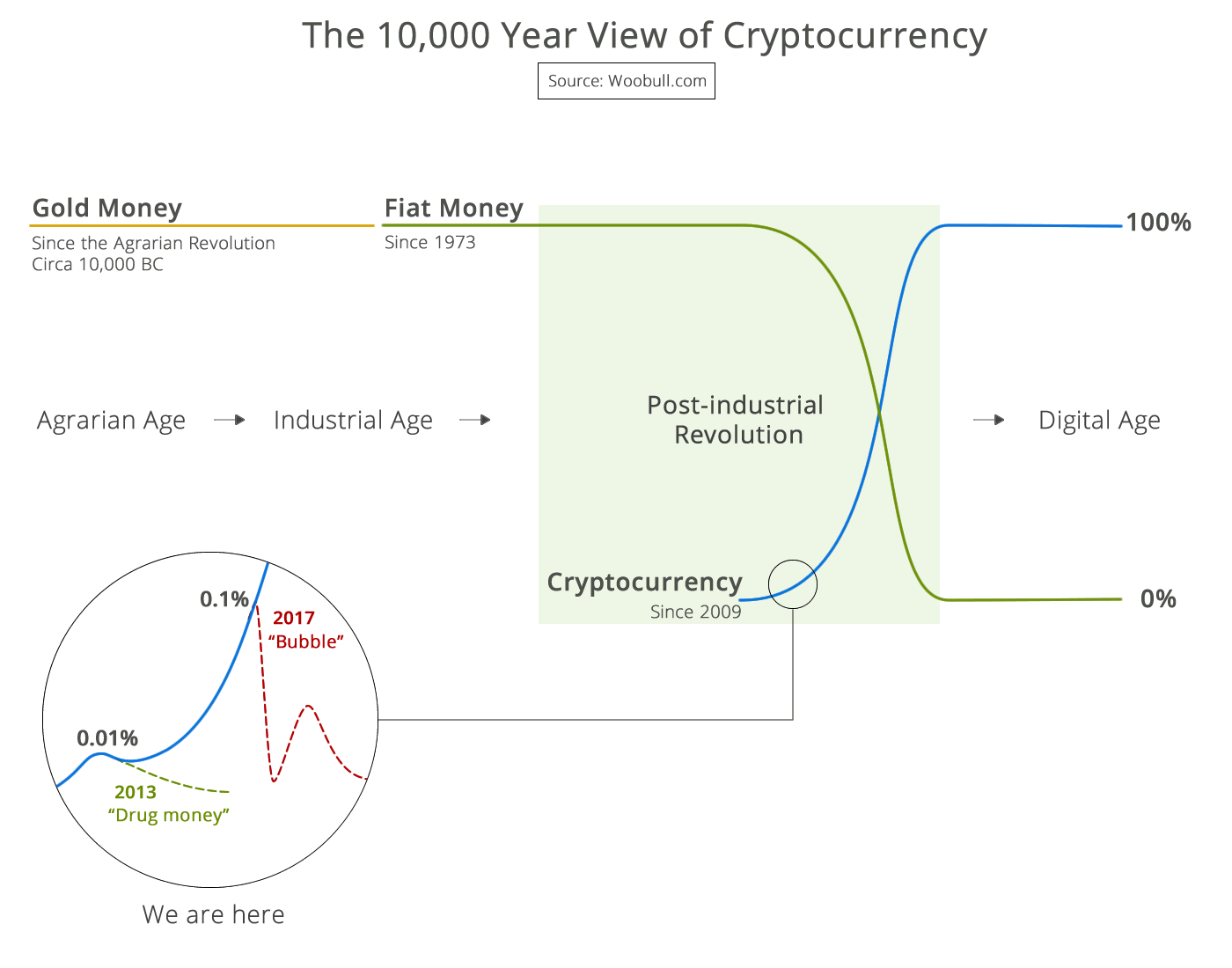

99% of ICOs Will Fail The 10,000 year view of cryptocurrency

The 10,000 year view of cryptocurrency