This blog entry has been moved and updated to the Increa Technology Wiki.

FAFSA stands for Free Application for Federal Student Aid. EFC stands for Expected Family Contribution. They’re terms any parent sending a kid to college knows very well. They’re suppose to help you and your children afford a college education. It’s become a socialized night-mare.

The idea is that you enter all your private financial information in the FAFSA web page, and then using formulas described in the EFC booklet, out pops the number your family is expected to contribute to your kids college. It doesn’t matter how much any college costs, $45,000 per year or $9,000 per year. If it’s more than your EFC, the colleges do a really good job of getting you 1) grants, 2) scholarships, 3) federal loans, or 4) authorized work on campus until what’s remaining for you to pay is equal to your EFC.

I was surprised at how large the EFC number is, so I started playing guessing games with the formula, testing out what would happen if I earned more or less money. I was surprised, and you will be, too!

Consider the marginal change if you earned an extra $100 per year. (If you don’t understand the concept of marginal taxes, you have to read about that first.) Here is the break-out of where the extra $100 goes:

25.00 Federal Taxes

9.30 State Taxes

7.25 Sales Tax

6.20 Social Security

1.45 Medicare

0.80 CA State Disability

——

$50.00 gone to taxes

The EFC marginal “tax rate” is 47% for anybody reporting more than $26,000 annual income. Check Table A6 in the EFC documentation linked above. In the $100 example, this leaves you with $3 for non-college expenses. To re-state it again for clarity, if you earn $100 more, you’ll spend $47 more on college expenses because the colleges will help you $47 less. $50 of it went to taxes. You’ll have $3 left for anything else. Why not earn a lot less and let the government pay for college? I’m done with overtime hours! This is a serious de-motivator to earn more money or get a better job! What are the federal legislators thinking?

I ran the example with 25% Federal tax bracket because that captures the actual Median Household Income in the years 1995 on up to today (bracket is $31K to $74K per year). If you make $74K to $155K per year, the Federal tax jumps to 28% and you get to spend none (zero dollars) of the $100 on non-college electives. If you are in a higher bracket, you loose non-college elective dollars if you earn more!

Some folks have winced when I include sales tax in the calculation. My observation is that nearly everybody spends the money they make each year. During college years, you’ll be lucky to not work in the red (spending more than you make). But if you’re really disciplined and stash all the money in the bank, you can keep the 7.25%. Well sort of. The EFC formula also measures how much you have saved in the bank, taking 5.6% toward college. See Line 23 on Page 9 of the EFC document linked above. If you try to save all of your pay raise, then pay taxes, and pay for college, you’ll be left with 4.65% or less in the bank.

Yippee.

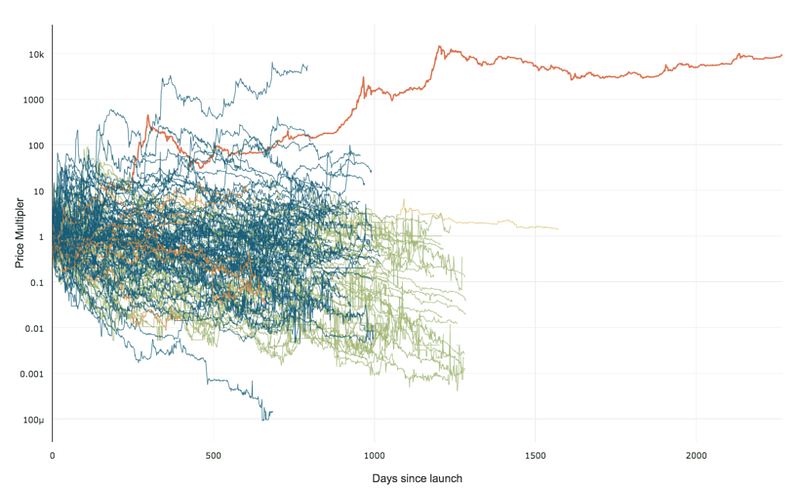

99% of ICOs Will Fail

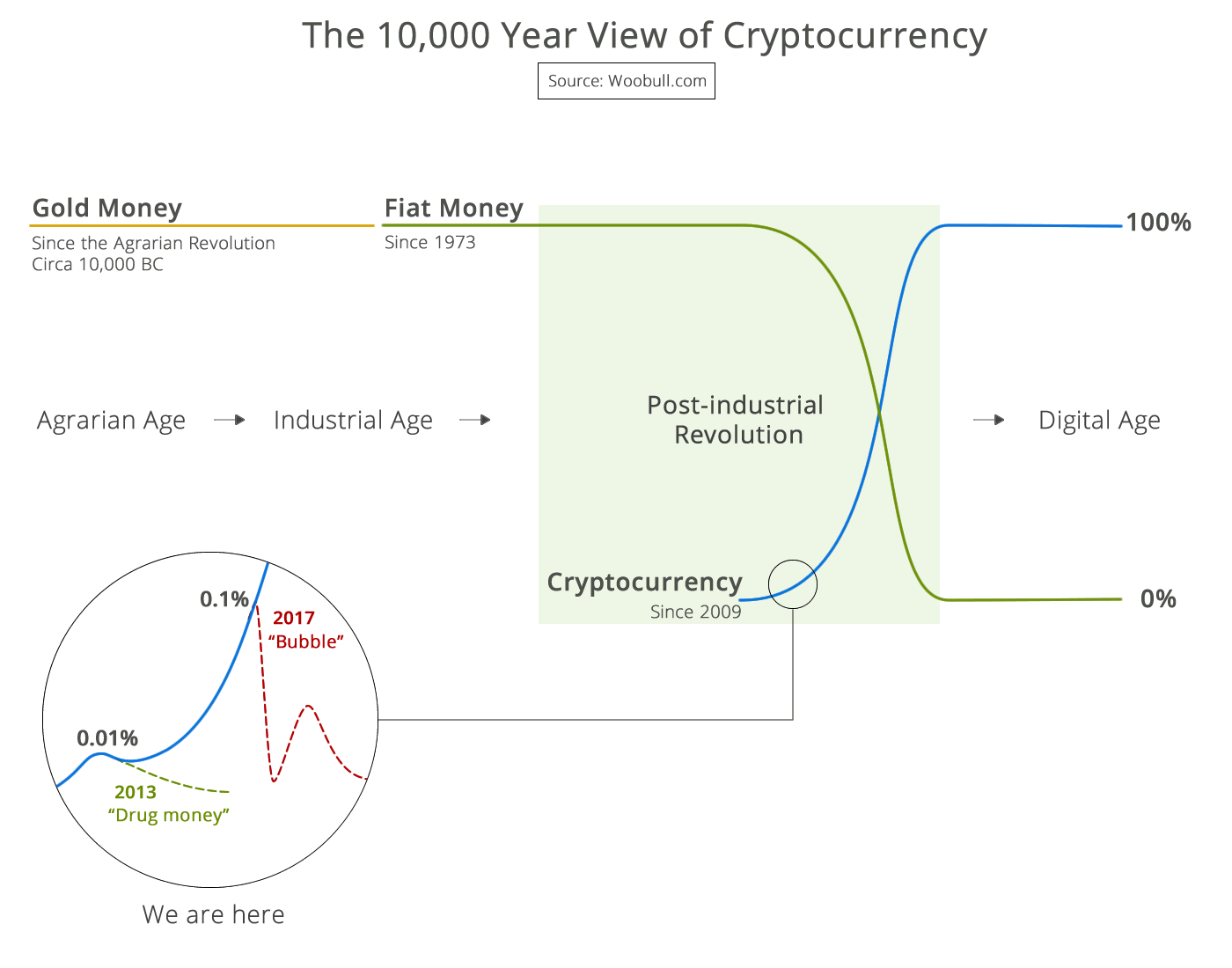

99% of ICOs Will Fail The 10,000 year view of cryptocurrency

The 10,000 year view of cryptocurrency